Saving for retirement is an important part of any budget, and if you work at a company that offers employees the opportunity to participate in a 401(k)-retirement plan, then you’re already two steps ahead.

To take it a step further, many companies that offer a retirement savings plan include employer match benefits, which means that your employer will match a percentage of your salary to your 401(k) contributions. So, when we ask if you’re turning down free money, we mean free money. Read on to learn more about employer match benefits, how you can increase your retirement nest egg quickly, and with little-to-no effort.

What is Employer Matching?

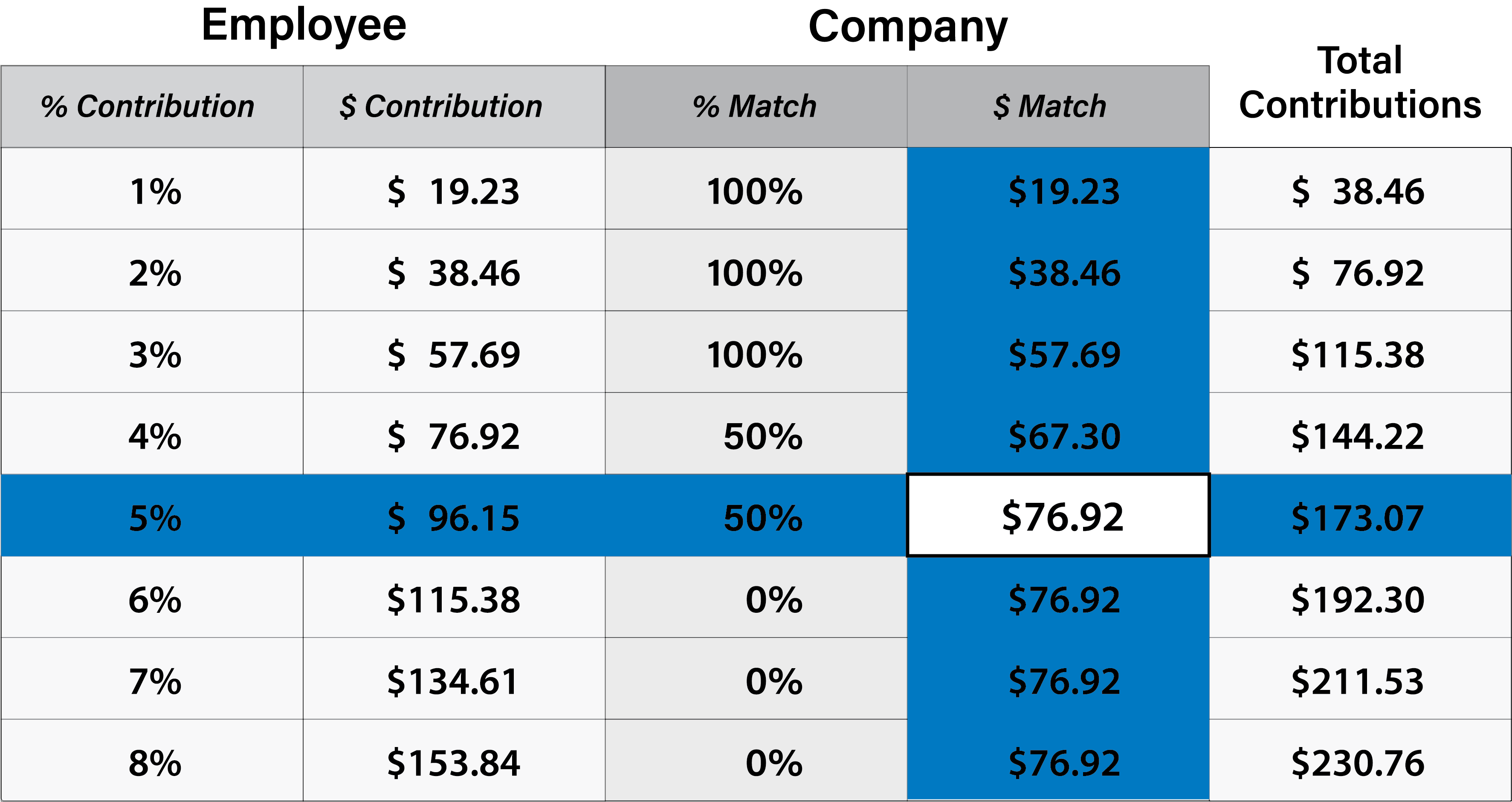

To put it simply, employer matching involves free money being contributed to your 401(k) by your employer. Depending on the terms of your employer’s 401(k) plan, your contributions may be matched up to a certain amount by your employer, which is usually a percentage of your salary or a specific dollar amount. For example, if your employer offers 5% in match dollars, then you too, should contribute 5%, doubling down on contributions to your retirement fund annually. But, if you only contribute 3%, then so will your employer. For high-earning employees, having a percentage match is more beneficial than a dollar amount, since they are typically a lot lower.

Regardless of how the plan is structured, if there’s free money available, take advantage! Talk to your company’s Human Resources department to learn about the options available to you.

Why Employer Matching is Important

From a business standpoint, employer matching is important because it attracts talent, increases 401(k) plan participation, improves employee retention, and can increase the financial well-being of employees. In a competitive business world, companies must stand out with their benefits packages, so make sure you inquire about employer matching during your interview process.

From a participant standpoint, matching is important because it doubles your retirement savings and provides tax benefits. Contributions made into a tax-advantaged 401(k) plan won’t be taxed until you withdraw the funds, and with pre-tax contributions, everything contributed to your 401(k) will reduce your current taxable income, saving you more money over time.

Maximizing 401(k) Contribution Limits

Maxing out retirement account contributions means that you’ve reached the limit determined by the Internal Revenue Service (IRS). The limit can change year-to-year, but in 2021 it was $19,500 for account holders under the age of 50. Enrollees over age 50 can continue to make contributions, called Catch-Up Contributions, up to $26,000.

In 2021, the IRS increased the joint contribution limit for the employer and the employee to $58,000 for people under the age of 50, and $64,500 for people over the age of 50. The total maximum contribution may not exceed 100% of the participant’s salary. You can visit the IRS’s website to learn more.

Know Your Company’s 401(k) Vesting Schedule

If you’re part of an employer-sponsored 401(k) program, your fund will eventually vest. Vesting means that you earn full rights to employer-provided funds over a specific amount of time. If your company’s vesting policy is two years, then you won’t have full ownership of the funds until you reach two years of successful employment. If you don’t, however, then your employer has the right to withdraw the funds they contributed prior to the two-year mark upon your resignation or dismissal. To encourage employee loyalty, employers commonly provide matching contributions to their employees’ retirement accounts with terms that limit how quickly the funds can be accessed.

Note that while employer contributions have vesting requirements, an employee’s own contributions are always 100% vested and cannot be forfeited to your employer. To learn more about vesting, visit the IRS.

If you find yourself opening the door to a new career, read our blog to learn what to do with your 401(k) when you change employers.

Saving for retirement doesn’t have to be frustrating or challenging. With personal savings and retirement accounts, as well as employer-sponsored accounts, you are well on your way to a healthy, financially stable future. Slavic401k offers multiple resources for its employer-sponsored investors, as well as free participant education tools. If you get stuck and have questions along the way, don’t forget to contact your company’s Human Resource team, and if you’re a Slavic401k participant, contact us here.